Caixin China General Manufacturing PMI (November 2020)

PMI hits highest level for a decade in November

Key findings

• Output and new orders both increase at fastest rates for ten years

• Employment expands at quickest pace since May 2011

• Improved demand drives substantial increase in purchasing activity

|

Data were collected 11-19 November 2020

Chinese manufacturers signalled the strongest improvement in operating conditions for a decade in November, as growth of both output and new orders accelerated to 10-year highs. The sustained and strong upturn in client demand led to the fastest increase in employment since May 2011. At the same time, firms raised their purchasing activity at the steepest rate since January 2011 and increased their inventories of both pre- and post-production goods. Greater market demand contributed to stronger inflationary pressures, however, with both input costs and output charges rising at sharper rates.

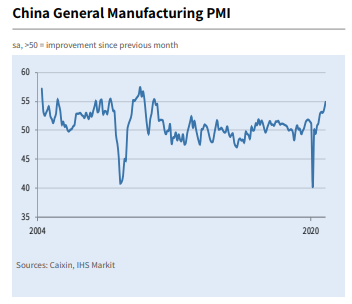

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – increased from 53.6 in October to 54.9 in November, to signal the sharpest improvement in conditions since November 2010. The health of the sector has now improved in each of the past seven months, to indicate a sustained and strong recovery from the coronavirus disease 2019 (COVID-19) outbreak earlier in the year.

Manufacturing companies in China recorded a sharp and accelerated rise in production during November, with the rate of expansion the quickest for 10 years. Firms frequently attributed the increase to greater new order volumes, as well as a further recovery from the COVID-19 related disruptions seen earlier in the year.

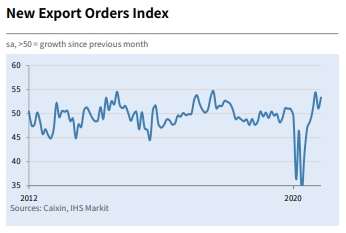

Overall sales likewise expanded at the quickest rate for a decade, which was often linked to a rebound in client demand. Underlying data suggested that the upturn continued to be led by firmer domestic demand, as growth in new export work was not as marked as that seen for total new orders.

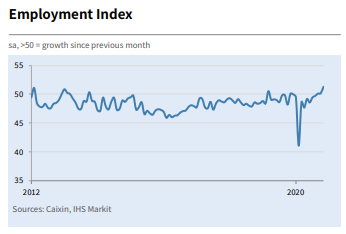

Increased production requirements and higher inflows of new work led companies to expand their workforce numbers again in November. Though modest, the rate of job creation was the strongest seen since May 2011. Capacity pressures persisted, however, as highlighted by a further rise in outstanding business. Furthermore, the rate of backlog accumulation was the quickest since April.

November data also revealed a substantial increase in purchasing activity, with the rate of growth the steepest since the start of 2011. However, the time taken to receive purchased inputs continued to lengthen amid reports of stock shortages at suppliers.

On the inventories front, stocks of purchases rose further in November, and at the fastest rate since February 2010. Inventories of post-production items meanwhile increased at a rate that, though marginal, was the quickest for 33 months. Panel members often attributed stock building efforts to improved sales and stronger overall market conditions.

Greater demand for inputs placed upward pressure on costs in November. Input prices rose sharply overall, with a number of monitored firms commenting on increased raw material costs, with metals mentioned in particular. Companies raised their selling prices at a quicker pace as a result, though the rate of increase remained below that seen for operating expenses.

Business confidence regarding the 12-month outlook for output remained strongly positive in November, despite easing slightly since October. Optimism was linked to planned company expansions, supportive state policies and hopes that global conditions will rebound once the pandemic ends.

|

|

Comment

Commenting on the China General Manufacturing PMI data, Dr. Wang Zhe, Senior Economist at Caixin Insight Group said:

“The Caixin China General Manufacturing PMI rose to 54.9 in November from 53.6 the previous month, the highest reading since November 2010. The Manufacturing PMI has now signaled an improvement in conditions for seven months in a row as the post-epidemic economic recovery continued to pick up speed.

1. Manufacturing continued to recover and the economy increasingly returned to normality as fallout from the domestic Covid-19 epidemic faded. Both demand and supply accelerated as the subindexes for total new orders and output reached 10-year highs. Overseas demand improved substantially as the measure for new export orders stayed in expansionary territory for the fourth month in a row, rising from the previous month. As production overseas was subdued by uncertainties brought by the pandemic, Chinese enterprises saw an increase in export orders. But the improvement in overseas orders was slightly weaker than that of domestic demand.

2. Employment continued to recover. The employment subindex stayed in expansionary territory for the third straight month as strong growth in supply and demand gradually exerted influence on the job market. Although employment’s expansion still lagged behind orders and output, the subindex hit the highest level since May 2011. More and more surveyed enterprises began adding staff to meet strong market demand.

3. There are clear signs that manufacturers were adding to their inventories. Growth in stocks of finished goods, quantity of purchases and stocks of purchases all accelerated, as the three measures reached their highest since February 2018, January 2011 and February 2010, respectively. Meanwhile, the active market led to longer delivery times from suppliers.

4. Inflationary pressures grew as prices rose at a faster pace. In November, the gauges for input and output prices rose further into expansionary territory. Respondents said a sharp rise in the prices of raw materials, especially metals, was a major reason behind the price hike. Strong demand coupled with a rise in costs pushed up factory gate prices further.

“To sum up, manufacturing recovered at a faster clip in November as supply and demand improved at the same time. Employment recovered markedly and overseas demand kept expanding. Manufacturing enterprises added to their inventories to meet demand and they were quite confident about the economic outlook for the next 12 months. The gauge for future output expectations stayed high.

“We expect the economic recovery in the post-epidemic era to continue for several months. At the same time, deciding how to gradually withdraw the easing policies launched during the epidemic will require careful planning as uncertainties still exist inside and outside China.”

Contact

Dr. Wang Zhe

Senior Economist

Caixin Insight Group

+86-10-8590-5019

zhewang@caixin.com

Ma Ling

Senior Director

Brand and Communications

Caixin Insight Group

T: +86-10-8590-5204

lingma@caixin.com

Annabel Fiddes

Associate Director

IHS Markit

T: +44 1491 461 010

annabel.fiddes@ihsmarkit.com

Bernard Aw

Principal Economist

IHS Markit

T: +65 6922 4226

bernard.aw@ihsmarkit.com

Katherine Smith

Public Relations

IHS Markit

T: +1-781-301-9311

katherine.smith@ihsmarkit.com

About Caixin

Caixin is an all-in-one media group dedicated to providing financial and business news, data and information. Its multiple platforms cover quality news in both Chinese and English.

Caixin Insight Group is a high-end financial research, data and service platform. It aims to be the builder of China’s financial infrastructure in the new economic era

For more information, please visit www.caixin.com and www.caixinglobal.com.

About IHS Markit

IHS Markit (NYSE: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers nextgeneration information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates. All other company and product names may be trademarks of their respective owners © 2020 IHS Markit Ltd. All rights reserved.

About PMI

Purchasing Managers’ Index™ (PMI™) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely watched business surveys in the world, favoured by central banks, financial markets and

business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends. To learn more go to ihsmarkit.com/products/pmi.html.

If you prefer not to receive news releases from IHS Markit, please email katherine.smith@ihsmarkit.com. To read our privacy policy, click here.

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to IHS Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without IHS Markit’s prior consent. IHS Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall IHS Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Purchasing Managers’ Index™ and PMI™ are either registered trade marks of Markit Economics Limited or licensed to Markit Economics Limited. IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates.

- PODCAST

- MOST POPULAR