Caixin China General Manufacturing PMI (January 2020)

PMI slips to five-month low in January

Key findings

Production and new work both expand at softer rates

Employment falls for first time in three months

Business confidence improves as trade tensions ease

|

Latest PMI data signalled the softest improvement in operating conditions across China's manufacturing sector for five months in January. Companies signalled slower increases in new orders and output, while payrolls fell for the first time since last October.

The latter was partly linked to attempts to reduce costs, as firms saw a solid increase in overall operating expenses at the start of the year. More cautious approaches were also taken in terms of purchasing activity and stocks of inputs and finished items, which all fell slightly in January. Factory gate prices rose only modestly, however, due to competitive market pressures.

On a more positive note, an easing of China-US trade tensions helped to boost business confidence regarding the 12-month outlook for output. Notably, optimism about the year ahead rose to its highest level for 22 months.

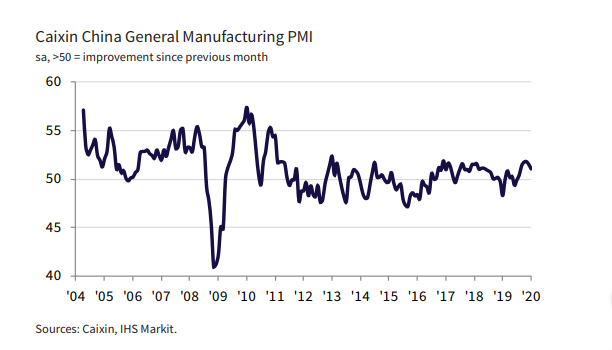

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a singlefigure snapshot of operating conditions in the manufacturing economy – edged down from 51.5 in December to 51.1 in January. Although remaining above the neutral 50.0 mark, the figure indicated only a marginal improvement in the health of the sector. Notably, the rate of mprovement was the slowest recorded since the rrent upturn began in August 2019.

Weighing on the headline PMI was a softer rise in new orders received by Chinese goods producers. The atest increase in new work was modest overall, with the rate of growth having eased for a third uccessive month. Data indicated that this was partly due to weaker external demand, as new export business fell for the first time in four months, albeit only slightly.

Reflective of the trend for new orders, output growth eased to a moderate pace in January. Moreover, the latest upturn in production was the softest seen for five months.

At the same time, some firms implemented down-sizing policies as part of attempts to reduce costs, which contributed to a renewed fall in employment. Concurrently, January data indicated an easing of capacity pressures, with backlogs of work broadly stable at the start of the year following a 46-month sequence of accumulation.

A cautious approach was taken in terms of buying activity. Following a six-month sequence of growth, purchasing activity fell slightly in January. As a result, companies reported a sligh dip in their inventories of pre-production stocks for the first time since last August. Inventories of finished items also fell marginally.

On the prices front, Chinese manufacturers recorded a solid increase in operating expenses. Firms often attributed higher input costs to greater prices for raw materials. Furthermore, the rate of cost inflation was the steepest recorded for 14 months. However, competitive market pressures limited the extent to which companies could pass on their cost burdens to clients, with selling prices rising only modestly at the start of 2020.

An easing of trade tensions between China and the US helped to lift business confidence to a 22-month high in January. Firms also attributed optimism to new product launches and expectations that global demand conditions will improve.

Comment

Commenting on the China General Manufacturing PMI data, Dr. Zhengsheng Zhong, Chairman and Chief Economist at CEBM Group said:

"The Caixin China General Manufacturing PMI stood at 51.1 in January, down from 51.5 in the previous month. The manufacturing sector expanded at the slowest pace since August, despite growing for six consecutive months, indicating a mild economic ecovery.

1) Manufacturing demand continued to grow at a slower rate, while overseas demand was subdued. The subindex for total new orders continued to weaken and dropped to a level not seen since last September. The gauge for new export orders fell into contractionary territory, ending three straight months of expansion.

2) Production growth slowed, with the output subindex posting its lowest reading since last August. The employment subindex returned to negative territory.

3) As slowing demand growth impacted production, suppliers’ delivery times lengthened, both stocks of purchased items and finished goods declined, and the gauge for backlogs of work dipped to a level just marginally above the dividing line between expansion and contraction, while staying in positive territory for nearly four years. These phenomena suggested that not every manufacturer replenished inventories despite an earlier recovery in production.

4) That said, business confidence continued to improve, with the gauge for future output expectations on the rise and tending to recover after two years of depression, due chiefly to the phase one trade deal between China and the U.S.

5) Industrial product prices continued to rise. As input costs grew at a faster pace than output prices, we need to pay attention to pressure on costs of raw materials.

"China’s manufacturing economy recovered at a slower pace at the start of the year. Although corporate confidence was boosted by the trade deal, some manufacturers did not replenish stocks despite the pickup in production, due to limited improvement in domestic and foreign demand. Pressure from rising raw material costs is worth attention. In the near term, China’s economy will also be impacted by the new pneumonia epidemic, and therefore need to gain support from proper countercyclical policies."

|

|

Survey methodology

The Caixin China General Manufacturing PMI™ is compiled by IHS Markit from responses to questionnaires sent to purchasing managers in a panel of around 500 private and state-owned manufacturers. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP. For the purposes of this report, China is defined as mainland China, excluding Hong Kong SAR, Macao SAR and Taiwan.

Survey responses are collected in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses. The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

The headline figure is the Purchasing Managers’ Index™ (PMI). The PMI is a weighted average of the following five indices: New Orders (30%), Output (25%), Employment (20%), Suppliers’ Delivery Times (15%) and Stocks of Purchases (10%). For the PMI calculation the Suppliers’ Delivery Times Index is inverted so that it moves in a comparable direction to the other indices.

Underlying survey data are not revised after publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series.

For more information on the survey methodology, please contact economics@ihsmarkit.com.

Survey dates and history

January 2020 data were collected 13-22 January 2020.

Data collection began in April 2004.

Contact

Dr. Zhengsheng Zhong

Chairman and Chief Economist

CEBM Group

T: +86-10-8104-8016

zhongzhengsheng@cebm.com.cn

Ma Ling

Senior Director

Brand and Communications

Caixin Insight Group

T: +86-10-8590-5204

lingma@caixin.com

Annabel Fiddes

Principal Economist

IHS Markit

T: +44 1491 461 010

annabel.fiddes@ihsmarkit.com

Bernard Aw

Principal Economist

IHS Markit

T: +65 6922 4226

bernard.aw@ihsmarkit.com

Katherine Smith

Public Relations

IHS Markit

T: +1-781-301-9311

katherine.smith@ihsmarkit.com

About Caixin

Caixin is an all-in-one media group dedicated to providing financial and business news, data and information. Its multiple platforms cover quality news in both Chinese and English.

Caixin Insight Group is a high-end financial research, data and service platform. It aims to be the builder of China’s financial infrastructure in the new economic era

For more information, please visit www.caixin.com and www.caixinglobal.com.

About IHS Markit

IHS Markit (NYSE: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers nextgeneration information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates. All other company and product names may be trademarks of their respective owners © 2020 IHS Markit Ltd. All rights reserved.

About PMI

Purchasing Managers’ Index™ (PMI™) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely watched business surveys in the world, favoured by central banks, financial markets and

business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends. To learn more go to ihsmarkit.com/products/pmi.html.

If you prefer not to receive news releases from IHS Markit, please email katherine.smith@ihsmarkit.com. To read our privacy policy, click here.

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to IHS Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without IHS Markit’s prior consent. IHS Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall IHS Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Purchasing Managers’ Index™ and PMI™ are either registered trade marks of Markit Economics Limited or licensed to Markit Economics Limited. IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates.

- 1Cover Story: Beijing Summit Signals a Reset in U.S.-China Relations

- 2China Evergrande Liquidators Sue PwC for $8.4 Billion Over Audit Work

- 3China Retail Sales Barely Grow as Consumer Demand Weakens

- 4German Rape Cases Expose Cross-Border Drugging Network Targeting Chinese Women

- 5Exclusive: China Steps Up Oversight of Bond Rating Terminations

- 1Power To The People: Pintec Serves A Booming Consumer Class

- 2Largest hotel group in Europe accepts UnionPay

- 3UnionPay mobile QuickPass debuts in Hong Kong

- 4UnionPay International launches premium catering privilege U Dining Collection

- 5UnionPay International’s U Plan has covered over 1600 stores overseas