Caixin Insight: China Imposed New Controls on Real Estate and Tech

Manufacturing, services continue expansion

The Caixin Services PMI fell slightly by 0.1 points to 54 last month, remaining in expansionary territory for the fourth month in a row. The index’s performance showed that the services sector continued to recover from the impact of Covid-19 as domestic spending on services rebounded, though overseas demand remained sluggish, with the measure for new export business staying in negative territory for the second consecutive month.

Both the manufacturing and services sectors saw improvements in employment. In services, increases in business activity and sales led companies to expand staffing for the first time in seven months, and the manufacturing employment measure reached its closest point to expansion since December.

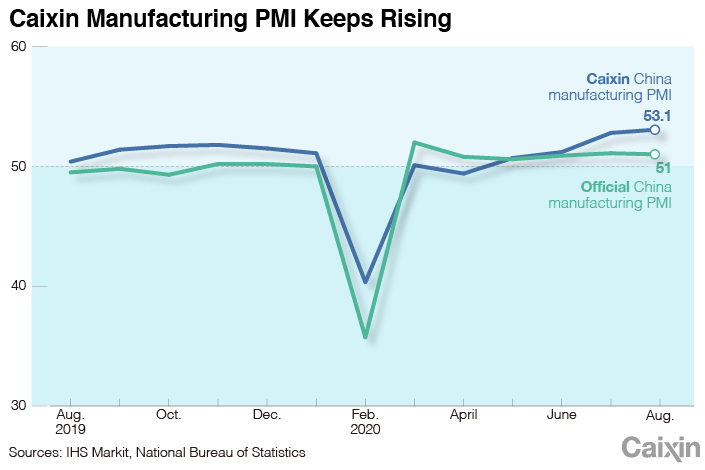

While services expansion decelerated slightly, manufacturing growth continued to accelerate, with the Caixin China Manufacturing PMI hitting an over nine-year high for the second straight month, rising to 53.1 last month from 52.8 in July, its highest point since the start of 2011. The index’s performance suggests the sector’s recovery may see strong momentum going into the latter months of 2020, as policymakers throw support behind manufacturing as a way to offset the pandemic’s impact and achieve policy goals around high-tech self-sufficiency.

|

Foreign companies can file more complaints

On August 31, China’s Ministry of Commerce (MOFCOM) set up a formal, legally codified complaint handling system for foreign-invested companies for the first time, in response to a requirement in the Foreign Investment Law. MOFCOM says the rules, which will take effect in October, aim to:

- ensure fair competition between domestic and foreign companies

- strengthen multinational companies' confidence in investing in China

- help China to build a market-oriented and law-based international business environment

The new system broadens the scope of complaints that foreign-invested enterprises can file, improves the complaint processing mechanism, and requires agencies to better protect complainants’ trade secrets, confidential business information, and other data submitted as part of complaints. It also shortens the complaint processing time limit from two years to one year and allows complainants who disagree with local decisions to appeal to high-level authorities.

Zong Changqing, director-general of the MOFCOM Department of Foreign Investment Administration, said in a press conference the new rules will help to establish a benign relationship between foreign investors and the Chinese government. Analysts have pointed out that they aim to provide foreign-invested companies with business opportunities that were once only available to domestic ones and implement WTO rules.

Real estate “redlines”

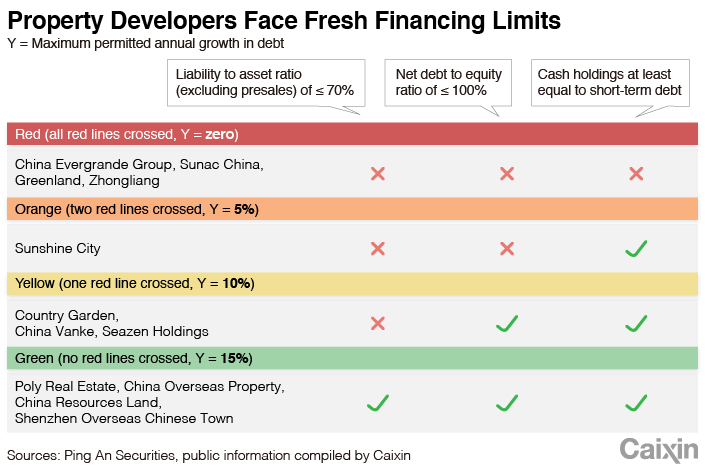

Real estate developers will reportedly soon be subject to new financing restrictions, currently being piloted by 12 firms. The new rules include three “redlines”: a liability-to-asset ratio (excluding presales) of no more than 70%; a net debt-to-equity ratio of under 100%; and cash holdings at least equal to short-term debt. Companies that do not overstep any of the three red lines will be able to increase their annual interest-bearing liabilities by up to 15%, while those that cross one or two red lines are allowed an increase of 10% and 5%, respectively. Developers that step over all three red lines will be barred from taking on more debt.

|

The policy is the latest attempt to stabilize leverage, get a handle on developers’ debt and stabilize the housing market. But there is always a regulatory gap: the stricter the explicit policy, the more likely it is that some companies able to take advantage of loopholes will be able to overtake others despite operating under the same limits. The new rules should be manageable for the biggest companies, but small and midsize property developers may suffer more, as the limits may effectively place a cap on growth and ossify the positions of top firms.

Tech export controls impact more than ByteDance

On August 28, China’s Ministry of Commerce and Ministry of Science and Technology revised a list of technologies subject to export restrictions for the first time in 12 years, with 53 revisions in total. Among the most notable additions to the restricted list were personal information push services based on data analysis and video-recognition technologies commonly used in smartphones, robots, and wearable devices.

Much of the attention to the policy has revolved around ByteDance, whose core technologies are on the list. The company has said it will strictly comply with the new policy, which will require it to get MOFCOM permission before it can conduct substantive negotiations, effectively putting the TikTok sale on hold until it’s received approval to move forward.

But ByteDance is, of course, not the only company impacted. DJI Technology, the world’s biggest drone manufacturer with an estimated 70% of the global market, will also need a license from MOFCOM before it can export its drones. DJI told Caixin that it must unconditionally comply with the decision, and that it is still assessing the impact on its business.

Although the sale of general tech products will not be affected, the list now covers licensing and transfer of intellectual property rights, as well as the transfer of complete production lines and equipment. The revision of the export list shows Chinese policymakers’ aim to tighten regulation, said a partner at another law firm specializing in intellectual property. The timing of the revision was clearly a response to the TikTok situation, but the scope and intensity of regulation are expected to expand, and companies like DJI will face similar regulatory scrutiny in the future, the lawyer said.

PBOC moves to improve benchmark interest rate system

On August 31, the PBOC released a white paper pledging to enhance its benchmark interest rate system ahead of the phase out of LIBOR at the end of 2021. China will make depository financial institutions’ repo rates (DR) a key reference to adjust monetary policy and price financial contracts, as it can better reflect the real liquidity situation in the banking system, according to the white paper.

Fifteen Chinese banks have carried out foreign currency-denominated services based on LIBOR pricing by the end of June, with a total value of $900 billion. These banks are facing a big challenge in the form of benchmark interest rate conversion and have to reevaluate liquidity and credit risks based on the new benchmark, according to a research report from PwC.

The PBOC said it has formulated a roadmap and timetable for domestic benchmark conversion and will help commercial banks shift from LIBOR to a self-designed interest rate system. This move will help China build up financial markets, deepen market-based interest rate reforms and improve the efficiency of monetary policy, it said.

In the future, the domestic benchmark interest rate system will shift from DR and HIBOR to DR, in line with the trend in the global market. However, DR and SHIBOR are not simple substitutes, as SHIBOR plays a significant role as a benchmark interest rate for longer term products ranging in term from 3 months to one year. Therefore, DR is unlikely to replace SHIBOR in the near future, according to Ming MIng, a senior analyst with CITIC Securities.

- 1Exclusive: China Widens Tax Net to Offshore Insurance

- 2U.S. Drafts Ban on Chinese Optical Modules, Exposing Mutual Supply Chain Risks

- 3In Depth: Former Shanxi Richest Man Indicted on Mafia, Casino Charges

- 4Caixin Explains: How China’s New Offshore Trust Rules Close Tax Loopholes

- 5Cover Story: China’s Drive to Shore Up Social Security Funds Brings a Payroll Shock

- 1Power To The People: Pintec Serves A Booming Consumer Class

- 2Largest hotel group in Europe accepts UnionPay

- 3UnionPay mobile QuickPass debuts in Hong Kong

- 4UnionPay International launches premium catering privilege U Dining Collection

- 5UnionPay International’s U Plan has covered over 1600 stores overseas