Caixin China General Services PMI (March 2022)

Services activity drops in March as virus containment measures tighten

Key findings

• Services activity falls at quickest rate since February 2020 amid notable drop in sales

• Input cost inflation picks up

• Business confidence softens to 19-month low

|

Data were collected 11-23 March 2022

The recent rise in COVID-19 cases in China and restrictions to limit the spread of the virus led to a marked drop in service sector activity at the end of the first quarter of 2022. The fall coincided with a steep decline in new work, which was often linked to restrictions on mobility and reduced customer numbers. Average input costs rose at an accelerated and solid pace, while prices charged by services companies rose only slightly. The ongoing pandemic and war in Ukraine meanwhile weighed on business confidence, which edged down to its lowest for just over a year-and-a-half in March.

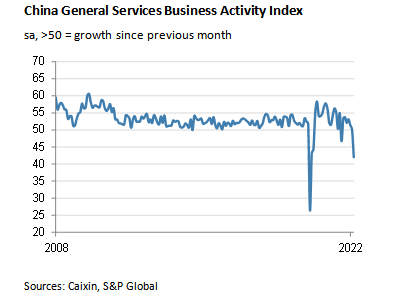

The seasonally adjusted headline Business Activity Index fell from 50.2 in February to 42.0 at the end of the first quarter, to signal a renewed contraction of services activity. Furthermore, the rate of reduction was the steepest seen since the initial onset of the pandemic in February 2020 and sharp. Businesses frequently mentioned that tighter virus containment measures had disrupted operations and weighed on client demand in March.

Chinese services companies registered a solid and accelerated fall in total new work at the end of the opening quarter. Notably, the rate of decline was the fastest since March 2020. Pandemic-related restrictions, notably those on mobility, were frequently attributed to lower customer numbers and softer demand conditions. New export business fell for the third month running. Though modest, the rate of decrease was the fastest since October 2020.

Staffing levels at services companies fell in March, as has been the case throughout the first quarter, though the rate of reduction was only fractional. Panel members indicated that the pandemic and softer demand conditions had reduced firms' appetite for additional staff.

At the same time, disruption to business operations led to a further increase in the level of outstanding business at Chinese service providers. Though mild, the rate of accumulation was the quickest seen since last December.

March survey data signalled a stronger rise in input costs faced by services companies. The rate of inflation was solid overall and quicker than the series average. Companies cited greater costs for raw materials, energy, food, transport and greater expenditure on pandemic-protection measures as having driven up cost burdens in the latest survey period.

Although expenses rose at a quicker pace, fees charged by services companies rose only slightly during March. Moreover, the rate of increase was the softest seen in the current seven-month period of inflation. While some firms raised their charges due to higher input costs, others mentioned that pricing power was limited due to subdued demand conditions and efforts to attract new business.

When assessing the 12-month outlook for business activity, Chinese services companies were generally upbeat that output would expand over the next year. However, the degree of optimism slipped to its lowest for 19 months amid concerns over how long business operations would be impacted by the pandemic, and the war in Ukraine.

|

Comment

Commenting on the China General Services PMI™ data, Dr. Wang Zhe, Senior Economist at Caixin Insight Group said:

“The Caixin China General Services Business Activity Index came in at 42 in March, down from 50.2 the previous month. The March reading was the lowest since February 2020. The latest wave of the Covid-19 epidemic hit China’s services sector hard.

“Both supply and demand in the services sector contracted sharply after the latest wave of Covid outbreaks started to take off in early March. The services PMI dropped to its lowest since February 2020, while the gauge of total new business dropped to its lowest since March 2020. Overseas demand remained weak, with the gauge of new export business falling to its lowest since October 2020.

“Services employment fell slightly. The measure for employment remained in contractionary territory for the third consecutive month. Amid the new wave of outbreaks, market demand was lacking and there was little motivation for enterprises to expand their operations and increase staff. As a result, the backlog of work in the services sector increased.

“Price gauges rose, increasing service enterprises’ costs. The gauge of input costs stayed in positive territory and rose, indicating that the increase in cost pressure accelerated. Labor costs and prices of raw materials, food and freight all increased. The gauge of prices charged was slightly over 50 in March and lower than the previous month, impacted by weak demand.

“Businesses grew less optimistic. Entrepreneurs were still confident that the epidemic would be brought under control eventually, but this optimism faded. In March, the measure for planned future activity hit a 19-month low."

|

Caixin China General Composite PMI™

Total business activity falls at quickest pace since February 2020

Composite indices are weighted averages of comparable manufacturing and services indices. Weights reflect the relative size of the manufacturing and service sectors according to official GDP data. The China Composite Output Index is a weighted average of the Manufacturing Output Index and the Services Business Activity Index.

The seasonally adjusted Composite Output Index fell from 50.1 in February to 43.9 in March, to signal a renewed and steep decline in total Chinese business activity. This signalled the first fall in output since last August, with the rate of reduction the quickest seen since the initial onset of the pandemic in February 2020. The reading reflected renewed falls in both manufacturing and services activity, with the latter noting the faster rate of decline.

Total new business likewise fell at the fastest rate for just over two years, with both goods producers and services companies noting marked falls in sales. Composite new export work also fell sharply, and at the fastest rate for 22 months. Business confidence subsequently softened in March, to reach its lowest since May 2020.

Cost pressures meanwhile intensified, with the overall rate of input price inflation accelerating to a five-month high, but prices charged inflation eased slightly.

Comment

Commenting on the China General Composite PMI™ data, Dr. Wang Zhe, Senior Economist at Caixin Insight Group said:

“The Caixin China General Composite PMI came in at 43.9 in March, down from 50.1 the previous month. Supply and demand in both manufacturing and services were under pressure. Overseas demand also recorded the worst performance since May 2020. The prices gauges remained in expansionary territory, indicating that business costs grew further. Employment was relatively stable. Businesses were less optimistic.

“Overall, both manufacturing and services activities weakened in March due to the epidemic. Similar to previous Covid outbreaks in China, the services sector was more significantly affected than manufacturing. Supply shrank, and demand was under pressure. Exports deteriorated. Businesses’ costs rose. Employment was more or less stable. Market optimism weakened.

“At present, China is facing the most severe wave of outbreaks since the beginning of 2020. Uncertainty also increased abroad. The outcome of the war between Russia and Ukraine is uncertain, and the commodity market has convulsed. Several factors have aggravated the downward pressure on China’s economy and underscore the risk of stagflation.

“Policymakers are facing double challenges of “precision” — improving the precision of epidemic control measures to strike a balance between maintaining normal life and guarding the people’s health; ensuring fiscal and monetary policy are implemented precisely. Policymakers should look out for vulnerable groups and enhance support for key industries and small and micro businesses to stabilize market expectations.”

Contact

Dr. Wang Zhe

Senior Economist

Caixin Insight Group

+86-10-8590-5019

zhewang@caixin.com

Ma Ling

Senior Director

Brand and Communications

Caixin Insight Group

T: +86-10-8590-5204

lingma@caixin.com

Annabel Fiddes

Associate Director

IHS Markit

T: +44 1491 461 010

annabel.fiddes@ihsmarkit.com

Joanna Vickers

Corporate Communications

IHS Markit

T: +44 207 260 2234

joanna.vickers@ihsmarkit.com

About Caixin

Caixin is an all-in-one media group dedicated to providing financial and business news, data and information. Its multiple platforms cover quality news in both Chinese and English.

Caixin Insight Group is a high-end financial research, data and service platform. It aims to be the builder of China’s financial infrastructure in the new economic era.

Read more: https://www.caixinglobal.com/index/

For more information, please visit www.caixin.com and www.caixinglobal.com.

About IHS Markit

IHS Markit (NYSE: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers nextgeneration information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates. All other company and product names may be trademarks of their respective owners © 2022 IHS Markit Ltd. All rights reserved.

About PMI

Purchasing Managers’ Index™ (PMI™) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely watched business surveys in the world, favoured by central banks, financial markets and

business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends. To learn more go to ihsmarkit.com/products/pmi.html.

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to IHS Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without IHS Markit’s prior consent. IHS Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall IHS Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Purchasing Managers’ Index™ and PMI™ are either registered trade marks of Markit Economics Limited or licensed to Markit Economics Limited. IHS Markit is a registered trademark of IHS Markit Ltd. and/ or its affiliates.

- PODCAST

- MOST POPULAR