China Carbon Watch (April): Trading Volume Doubles Previous Month’s Record Low

Carbon market update

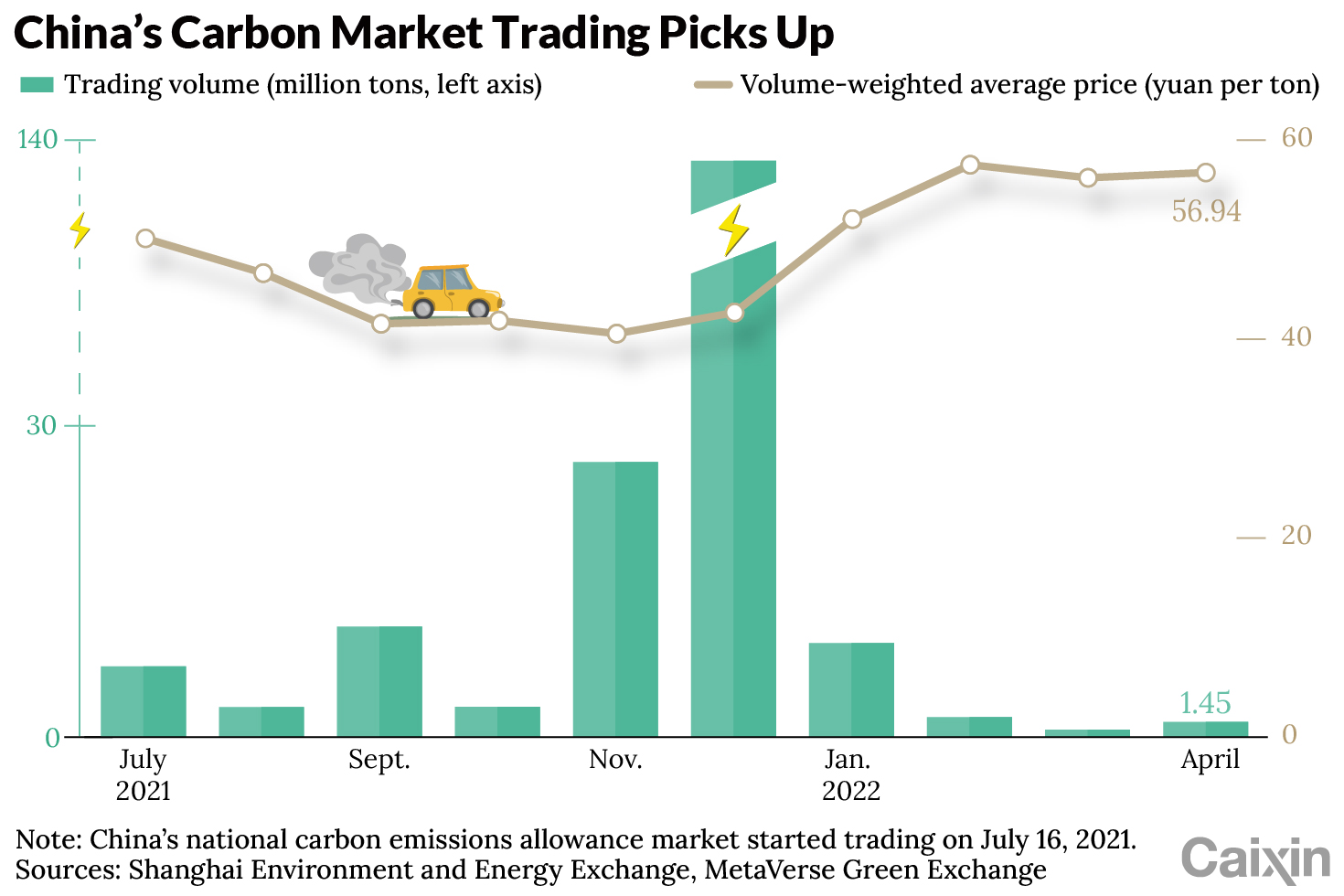

April’s trades in China’s national carbon emissions allowance (CEA) market ended with a total monthly volume of 1.45 million tons, more than doubling the all-time low of March. This volume, however, is still the second lowest on record, reflecting the lack of incentives for market participants to actively engage in the market.

Block trades were seen on six of the 19 trading days, accounting for 96.9% of the monthly total volume.

|

Market prices held up well amid low volumes, with open market transactions closing April at 58.80 yuan ($8.90) per ton, up 0.43% from a month earlier. Since the start of 2022, daily closing prices have remained over 56 yuan per ton, well above the 2021 average of 46.61 yuan per ton.

The April monthly volume-weighted average price for all trades was 56.94 yuan per ton, up 0.94% from March, pushed up by a 1.79% increase in the average block trade price.

Market news

• Zhang Xiliang, director of the Institute of Energy, Environment and Economy at Tsinghua University, said he expects the much-anticipated Interim Regulation for the Management of Carbon Emissions Trading to be published in 2022, according to an interview with digital media outlet Jiemian. The rules would give regulators more power and tools to ensure emission data quality for the market.

Zhang, who is widely considered the architect of China’s CEA trading system and its marketplace, also expects an auction system for allowances distribution to be introduced for the third compliance cycle for the CEA trading system beginning in 2023, alongside the inclusion of more covered industrial sectors and participation of financial players in the market.

Carbon news

• A study published by a leading domestic exchange for Chinese certified carbon emission reduction credits, or CCER credits, estimates that there will be a demand of about 4.1 billion tons of CCER credits from three sources by 2030. According to the Tianjin Climate Exchange, the current three main sources of demand for CCER credits are: China’s national CEA market, the CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation), and the international voluntary carbon offsetting market.

On the supply side, cumulative CCER credit supply may be close to 4.3 billion tons by 2030, which is roughly equal to the estimated demand. The estimate takes into account potential new credit-eligible projects under conservative assumptions for credit quantification, while adding existing registered credits and approved credit-eligible projects.

Bai Bo is executive chairman and co-founder of the Singapore-based MetaVerse Green Exchange.

The analysis and opinions expressed in third-party articles are those of the authors and do not necessarily reflect the positions of Caixin.

Contact editor Bertrand Teo (bertrandteo@caixin.com)

Download our app to receive breaking news alerts and read the news on the go.

Get our weekly free Must-Read newsletter.

- RELATED

- PODCAST

- MOST POPULAR