Analysis: Stricter Regulations Challenge Ant Group and Fintech’s Rapid Rise

The abrupt suspension of Ant Group Co. Ltd.’s potentially record-shattering $34.5 billion IPO in Shanghai and Hong Kong has sent shockwaves through the fintech industry, as China is poised to lay out a stricter regulatory framework to control financial risks and further protect the rights and interests of consumers.

That leaves the businesses of many fintech firms — especially those heavily reliant on online lending — hanging in the balance.

Stricter lending regulation

On Monday, China released draft rules (link in Chinese) that would require stricter standards for online microlenders. The draft rules will likely hamper Ant Group’s expansion as regulators treat fintech firms like Ant Group more and more like traditional financial firms.

E-commerce tycoon Jack Ma’s Ant Group relies heavily on its online lending business. It runs what’s considered to be the country’s largest online consumer credit platform through its Huabei (花呗) and Jiebei (借呗) products, which offer unsecured loans, according to its IPO prospectus.

Ant Group’s expansion could be hindered as the draft specifies that online microlenders should themselves fund at least 30% of any joint loan with financial institutions. However, as of the end of June, Ant Group’s licensed nonbank financial subsidiaries contributed only 2% of more than 2.1 trillion yuan ($313 billion) in the credit balance enabled through its platform, according to the prospectus.

The regulators also aim to limit the amount of leverage that online microlenders can take on. The draft stipulates that their nonstandardized debt such as bank loans must not exceed their net assets, while their standardized debt like bonds should not exceed their net assets by a multiple of four.

Such restrictions may force Ant Group to change the way it raises money to fund its Huabei and Jiebei products.

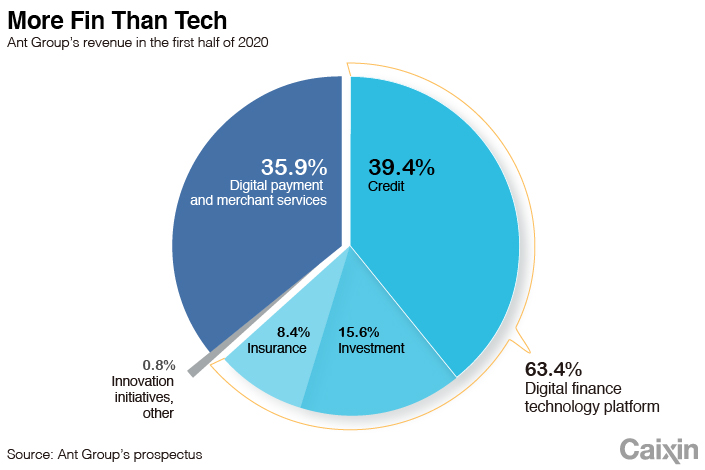

The proposed regulations, if approved in their current form, have the potential to create headaches for Ant Group — at least in the short term — as online lending has become a major driver of income, contributing nearly 40% of its total revenue in the first six months of this year, according to the prospectus. That’s more than its stalwart payment business, which accounted for 36% of revenue during the same period.

|

New regulatory regime

Ant Group is now also subject to stricter capital requirements under a new rule for financial holding companies that took effect on Nov. 1, which would slow what has so far been rapid growth.

In recent years, the company has repeatedly emphasized that it is a technology-driven company, even though its revenue has mainly been generated by its financial businesses, including payment and online lending. Its rapid expansion was in large part due to regulatory arbitrage, or rather its ability to sidestep some of the more stringent requirements for traditional financial institutions.

Regulators warned that de facto financial holding companies have expanded blindly, causing mounting risks to the financial system.

The new rule now requires nonfinancial companies that control businesses across at least two segments of the financial industry to get licensed as financial holding companies, in order to better supervise their businesses and manage potential risks. These companies are required to set aside at least 50% of the combined registered capital of the financial entities they control as actual paid registered capital, which should be at least 5 billion yuan. Regulators also demand their capital reserves match their asset size and risk levels.

That creates a hurdle for Ant Group to expand its financial businesses as it must be able to come up with enough money to cover its registered capital, let alone that it has to set aside large sums to comply with the new rule.

In September, Ant Group said (link in Chinese) that it planned to apply for a financial holding license for Zhejiang Finance Credit Network Technology Co. Ltd., the subsidiary under which Ant Group put three of its financial entities.

However, a string of other lucrative financial units that contribute a huge portion to its revenue exist outside Zhejiang Finance. They include subsidiaries that run Huabei, Jiebei, money-market fund Yu’e Bao and the consumer finance business.

Read more

Cover Story: How Ant Grew Into an Elephant-Sized Behemoth

Privacy and monopoly concerns

User data is a gold mine for Ant Group. But the business could face greater headwinds as regulations tighten and privacy laws curb how data get collected and used.

Over the past years, the huge customer base of online lenders has provided Ant Group with a vast ocean of information that it could mine through big data analytics and use to run targeted ads or assess its customers’ creditworthiness for loans. Such personal information can include customer names, phone numbers, addresses, fingerprints and facial features (used in facial recognition), as well as records of their purchases and the IP addresses of their smartphones and computers.

Last month, China’s top lawmakers deliberated on a draft personal information protection law that would levy big fines against those who illegally handle the information.

In addition, Ant Group’s dominance in online payment and lending has also sparked monopoly concerns. The new draft rules on online microlending reflect China’s strategy to foster fair competition in the market by curbing the wild expansion of lenders.

Overall, the stepped-up regulatory challenges facing Ant Group could also serve as a warning to its fintech peers, especially those controlled by internet titan Tencent Holdings Ltd. and e-commerce giant JD.com Inc. Apparently, regulators are seeking to put them on an even playing field with traditional financial institutions.

Ant Group’s IPO suspension is meant to give it more time to further disclose the impacts of new regulations on its business and valuation, said Iris Tan, a senior equity analyst at U.S. financial services firm Morningstar Inc.

“There’s no impact on opening capital market to foreign investors, but foreign investors should bear in mind there are plenty of regulatory risks in China as the regulations are evolving to catch up with the rapidly-growing fintech business,” Tan said.

Contact reporters Tang Ziyi (ziyitang@caixin.com) and Timmy Shen (hongmingshen@caixin.com) and editor Michael Bellart (michaelbellart@caixin.com)

Download our app to receive breaking news alerts and read the news on the go.

- RELATED

- PODCAST

- MOST POPULAR