In Depth: What Could Stop the Hottest Thing in IPOs From Landing in Hong Kong

Before New Frontier Health Corp. became the U.S.-listed company behind high-end hospital chain United Family Healthcare in China, it had existed for a time as little more than a shell of a corporation called New Frontier Corp.

New Frontier Corp., known as a special purpose acquisition company, or SPAC, had no underlying operating business until it acquired the hospital chain in 2019. It was a deal that effectively turned United Family Healthcare into a publicly traded company.

This is how many companies go public these days. Rather than applying to list on stock exchanges and going through a disclosure process, companies seeking an IPO instead negotiate a deal with an already listed SPAC, a company created for the sole purpose of taking another firm public.

Back in 2018, not many people in Asia knew about SPACs, said Lee Chen Kwok, an executive at investment bank UBS AG, which had advised New Frontier Corp. on the SPAC deal.

That was then, but Asian financiers have become familiar with the companies since the boom in SPAC IPOs began last year in the U.S., including Bridgetown Holdings Ltd. backed by PayPal Inc. co-founder Peter Thiel.

In Europe, Amsterdam’s Euronext stock exchange is fast becoming a prime spot for SPACs, with four SPACs getting listed from 2020 to early 2021, according to Intertrust Group, a company administration services provider.

In Asia, the pace of SPACs has been picking up in South Korea, ratings agency S&P Global Inc. wrote in a June report. And in June, the Hong Kong government said the city’s stock exchange would begin accepting public comments in the third quarter of this year about whether to allow SPACs.

Despite their growing popularity, allowing SPACs in Hong Kong will be no easy feat as the city’s securities regulator is concerned about shell companies being used to manipulate the market, such as through pump-and-dump stock schemes. And some observers (link in Chinese) are looking at to what extent the rules the city’s regulators will come up with can retain the flexibility and certainty that made SPACs so popular in the first place.

A shortcut to going public

As a fondness for SPACs grows in global financial markets, Hong Kong investors generally agree that it is necessary for the city’s stock exchange to introduce the investment and financing vehicle, said Mary Leung, head of standards and advocacy for the Asia Pacific region at the CFA Institute.

Hong Kong Exchanges and Clearing Ltd. (HKEX), the company that runs the city’s stock exchange, is looking to have the first SPAC listing within 2021, a report released by the Hong Kong Legislative Council said, citing local media Radio Television Hong Kong.

A SPAC is a newly created company that raises capital through an IPO to fund the acquisition of a privately held company. The SPAC’s management team needs to complete an acquisition within a period, typically within 24 months.

The U.S. Securities and Exchange Commission (SEC) calls SPACs “blank check companies” because they are essentially shell companies when they go public, holding no assets other than cash and limited investments.

Observers see advantages that the SPAC approach has over conventional IPOs. SPACs provide companies with access to capital even when market volatility and other conditions limit liquidity, PwC wrote in a note. SPACs could also potentially lower transaction fees and reduce how long it takes to list.

SPAC mergers provide certainty on the pricing of a would-be public company’s shares because the valuation is in large part by negotiations between SPAC founders and the acquisition target company that typically occur months before the transaction closes, while pricing for a traditional IPO is influenced by market volatility and investor sentiment, which “can vary significantly leading up to the time of pricing,” Deloitte China analysts wrote in a report.

The SPAC listing spree in 2020 was driven by abundant capital in the hands of private equity investors and by rising market volatility amid the Covid-19 pandemic, which prompted some companies to forego the conventional IPO route for something with more certainty, the Deloitte analysts wrote.

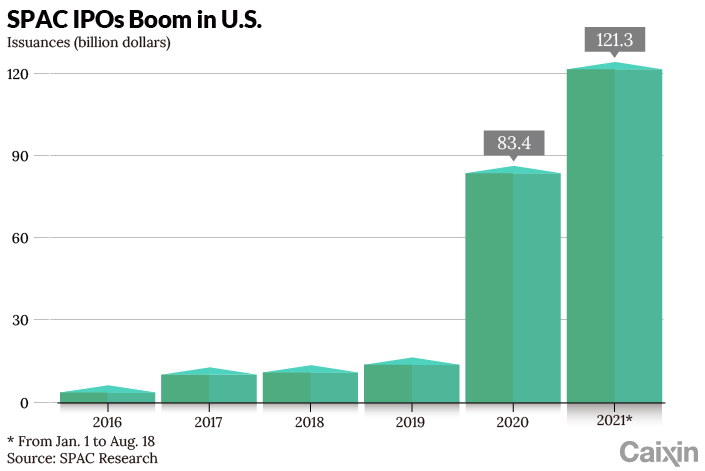

Last year, proceeds from SPAC IPOs in the U.S. surged to $83.4 billion from $13.6 billion in 2019, according to data from SPAC Research, an industry database.

|

Hong Kong challenges

Several obstacles stand in the way of SPACs taking off in Hong Kong, stemming from the tough stance that the city’s regulators have taken toward backdoor listings, which like SPACs involve a company going public through a shell corporation, some analysts said.

In 2019, the Hong Kong bourse tightened the rules on shell companies, saying that activities involving shell companies can invite speculative trading, lead to market manipulation and insider trading, and undermine investor confidence in the market.

Because the process of a SPAC acquiring a company isn’t all that different from a company going public by buying a listed shell company, it will be difficult for the city to allow SPAC IPOs, said Marcia Ellis, global chair of the private equity group at law firm Morrison & Foerster LLP.

There are concerns in the financial industry that allowing SPAC listings may run counter to regulators’ efforts to combat backdoor listings and shell companies, according to the Legislative Council report. Still, the report acknowledged that the current regulatory framework allows for some flexibility as Hong Kong Financial Secretary Chan Mo-po has said that the local securities watchdog and HKEX have been entertaining the possibility of a “Hong Kong version” of listing regime for SPACs.

If Hong Kong does end up allowing SPAC listings, regulators will likely impose strict rules on them, according to some analysts.

Analysts and global regulators have raised the alarm about risks posed by SPAC listings. Because a SPAC registration statement is not as detailed as an IPO prospectus, it leaves more leeway for hiding information and fraud, according to a report released by a research institute of Bank of China (Hong Kong) Ltd.

Last month, the U.S. SEC announced charges against Stable Road Acquisition and several other involved parties for making misleading disclosures ahead of the SPAC’s proposed acquisition. “This case illustrates risks inherent to SPAC transactions, as those who stand to earn significant profits from a SPAC merger may conduct inadequate due diligence and mislead investors,” SEC Chair Gary Gensler said in a statement.

Read more

Hong Kong Exchange May Join the SPAC Parade

HKEX will likely create strict approval standards for SPAC listings and may demand intermediaries in the deal like investment banks, law firms and accountant firms be held accountable when risks emerge, said Wong Wing Cheong, a partner at law firm Gallant.

However, tight SPAC rules may make the market less attractive because they would take away much of flexibility and certainty that have made SPACs so popular, according to some observers.

For example, Singapore Exchange Ltd. intends to adopt stricter SPAC rules than those in the U.S., including measures that would make it less likely for a SPAC acquisition to be approved, thereby reducing the certainty (link in Chinese) in the mechanism, Morrison & Foerster partners wrote.

Access to retail investors

Because investor protection is a crucial concern of Hong Kong’s financial regulators, some are speculating whether they would allow retail investors to participate.

Limiting SPACs to institutional and professional investors could strike a good balance between enhancing Hong Kong’s competitiveness as a fund raising hub and protecting mom-and-pop investors, according to an Asia Business Law Journal article in June that cited Gilbert Li, Hong Kong-based corporate partner of law firm Linklaters LLP.

In the U.S., retail investors are allowed to invest in a SPAC when it files for IPO through buying units. In a world of low interest rates, SPACs can serve as a desirable alternative for retail investors flush with cash as they allow access to companies that otherwise would likely have gone through rounds of venture capital funding before entering public markets, Michelle Heisner, an attorney at law firm Baker McKenzie, wrote in a commentary.

While SPACs have made money for some investors after their IPOs, they have also lost some investors money after they merge. According to a study published in January by three researchers from the University of Florida and the University of South Carolina, investors in 151 surveyed SPAC IPOs from 2010 to 2018 in the U.S. earned an average annualized return of 12% during the SPAC period. However, for the 114 SPACs that completed a merger from January 2012 to September 2020, investors lost an average 7.3% following the merger in the first year.

SPACs may be a high-risk investment for investors because they involve putting money into a company with no past financial performance and no business plan at the time of IPO, the Hong Kong Legislative Council report noted. Also, because a SPAC’s management team is typically rewarded with a stake in the new company created after the merger — usually about 20% — they have a perverse incentive to complete any acquisition available, regardless of the financial prospects of the target company, the report said.

Contact reporter Guo Yingzhe (yingzheguo@caixin.com) and editor Michael Bellart (michaelbellart@caixin.com)

Download our app to receive breaking news alerts and read the news on the go.

Get our weekly free Must-Read newsletter.

- RELATED

- PODCAST

- MOST POPULAR