Weekend Long Read: The Headaches Plaguing China’s Exporters and How They Are Hurting Trade

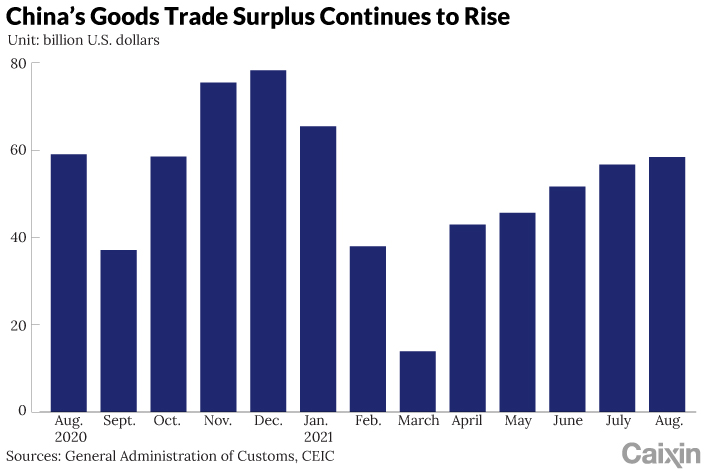

This year, we have witnessed the post-pandemic recovery of the global economy. Despite various challenges, such as the recovery of global production, the decline of overseas demand and the weak U.S. dollar index, China has maintained rapid, although somewhat fluctuating, growth in exports in the first half of 2021, with the monthly export volume continuously rising beyond the market expectations.

There are two reasons for this surge. The first is that the structural adjustments in export products have continued and major exports have shifted from anti-epidemic supplies and consumer durables to intermediate goods necessary for resumed global production. The second reason is that China has expanded its exports to emerging markets, especially to Southeast Asia.

|

However, some worrying signs has started to appear. The year-on-year ratios of the seasonally adjusted exports and the export delivery value have shown a slowing trend since April. The global export rebalancing will lead to a shift from Chinese production to global production. In addition, the full resumption of the overseas economies will drive the substitution effect of the overseas supply and demand.

Foreign trade and foreign-invested companies in China are important parts of its economy. Our survey shows that they are faced with four major challenges today, which will put pressure on foreign trade growth in the second half of 2021.

Headache 1: Shipping blockage

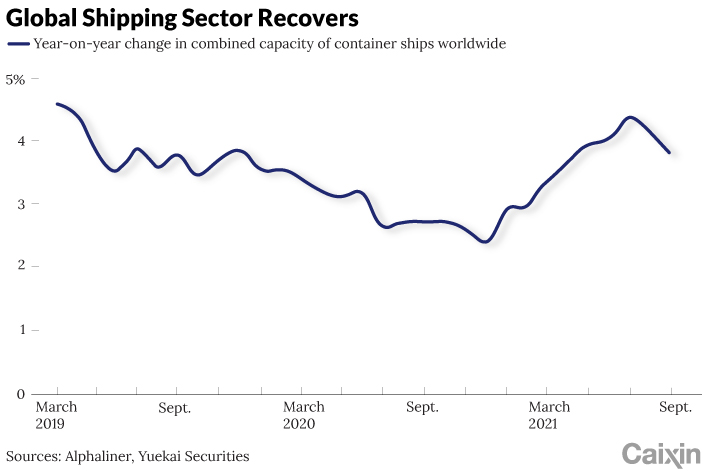

For foreign trade companies, shipping is the most important mode of transportation for goods. Over the past year, the international shipping sector has seen an increase in demand and shortage of supply, hurting China’s exporters and importers.

The worldwide spread of COVID-19 and the short supply of crew have resulted in the reduced capacity of cargo ships along the international routes. Meanwhile, the global economy and foreign trade demand have generally recovered, causing a supply-demand imbalance that raises freight rates. In addition, ports have introduced stricter pandemic prevention and control measures for people and goods, actively weakened their handling capacity and lengthened the clearance time, resulting in reduced shipping efficiency. Especially noticeable is the issue of closed hub ports, as this forces cargo ships to take longer routes, possibly causing the break of the entire shipping chain.

|

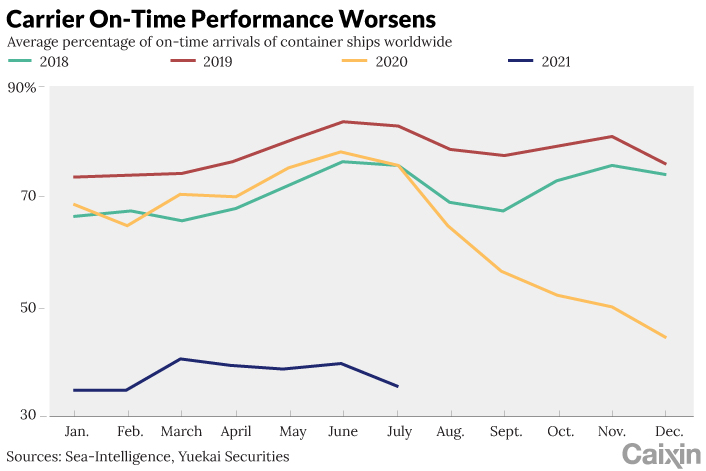

The global cancellations and delays for ocean shipping routes have gone up. Since the beginning of the year, freight charges have skyrocketed, while the on-time delivery rate (OTDR) has declined. In August, the spot rates for the routes from Shanghai to New York and to Los Angeles soared, with an increase of over 10%, more than doubling; the spot rates for major routes to Europe increased by more than 3% compared to the previous month, more than five times year-on-year.

According to Sea-Intelligence’s report, the OTDR of shipping companies around the world has been around 40% since March 2021, but it dropped to 35.6% in July, close to the low level at the beginning of the year. In July, the average OTDR of China’s major coastal ports has even gone below 20%.

|

As a result, the continuous rise in freight rates will squeeze their profits. Notably, small and midsize companies lack protection from long-term agreements, making it difficult for them to get deliveries on time, causing them to get caught in delays which further trigger inventory backlog and cash flow shortage. Because of this, they find themselves in a dilemma where they dare not receive orders as they cannot make profit from exports.

Headache 2: Short supply of materials

Key materials for the products of Chinese foreign trade companies are in short supply, thanks to the unstable industrial transfer and Covid-19.

For one thing, amid Covid-19, developed economies like the United States have imposed stricter restrictions and protection on strategic industries and sensitive sectors. Chinese foreign trade and foreign-invested companies have been deeply engaged in the international production network, making them more dependent on the resilience and stability of the supply chain. In particular, when it comes to high-tech firms, the industrial policies have been restrained by the global economic and trade landscape. Therefore, many companies are making efforts to improve their stocks of key parts and components and further diversify supply channels while transferring production bases closer to home and implementing production transfer in different regions.

The duration of the Covid-19 impact has been beyond expectations. The short supply of semiconductor chips has had an especially great impact on enterprise production.

For example, the short supply of chips of upstream enterprises has given rise to the shutdown or production reduction of downstream carmakers. IHS Markit predicted that nearly 1 million vehicles would be facing forced delays in the first quarter of 2021. According to AlixPartners, the impact of chip shortage will cause an income loss of $60.6 billion to the global automobile industry in 2021. Malaysia is a major manufacturing region for semiconductors. In August, Malaysia’s intensified pandemic situation led to the shutdown of some VCU chip lines for electric vehicles, further affecting foreign trade in automotive electronics. The supply-demand imbalance caused by Covid-19 cannot be resolved in a short time.

In the long run, to secure the national industrial chain, simultaneous layouts at home and abroad should be made to address the raw material issue.

Read more

Q&A: How One Foreign-Invested Firm Is Doing in China

Headache 3: Price surge

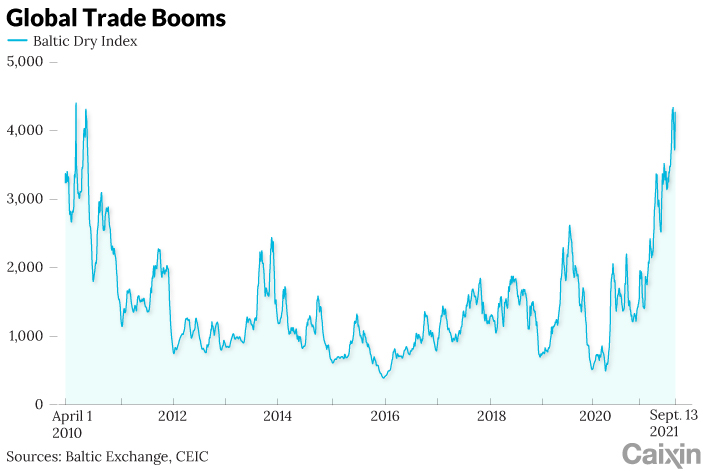

For foreign trade companies, the rise in prices of bulk commodities has pushed the prices of industrial raw materials up, lowering the profits of exporters at the production end. The central government has issued a number of policies, such as the promotion of import diversification and the establishment of stable channels for bulk commodities, to stabilize foreign trade.

The general rise in prices of bulk commodities since the beginning of the year has been driven by the global supply-demand imbalance and mobility. The Baltic Dry Index (BDI) is a typical indicator for global trade. The continuous rise of BDI is mainly attributed to the price surge of bulk commodities. In particular, the prices of black commodities, such as coal, have been rising, which has led to continuous new highs of freight rates.

|

Multiple factors like the decline of coal imports and short supply of domestic coal have lead to a negative supply-demand relationship in the domestic coal market, leading to the sustained high level of the coal price in the first half of this year. To control the coal price, national authorities including the National Development and Reform Commission (NDRC) have implemented several measures over the past two weeks to increase the coal capacity and comprehensively implement new strategies for the low-carbon energy transition.

Headache 4: Workforce crunch

Foreign trade companies have played an important role in stabilizing Chinese employment. But the current demographic trend has caused an irreversible rise in labor costs.

The post-pandemic labor market in China is facing a more prominent structural shortage of laborers. Foreign trade companies, especially cost-driven processing companies, are the worst affected.

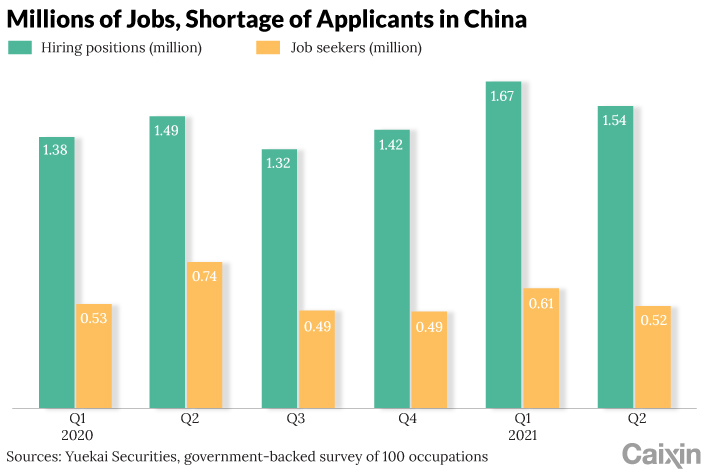

Since the outbreak of the pandemic, China’s labor shortage has worsened, especially in the manufacturing industry. According to the list of the top 100 occupations with the most acute shortage of labor released by the Ministry of Human Resources and Social Security, as of the second quarter of 2021, the employment gap (recruitment needs minus the number of applicants) increased rapidly, from 850,000 in the first half of 2020 to 1,021,000, a rise of 20.1%.

|

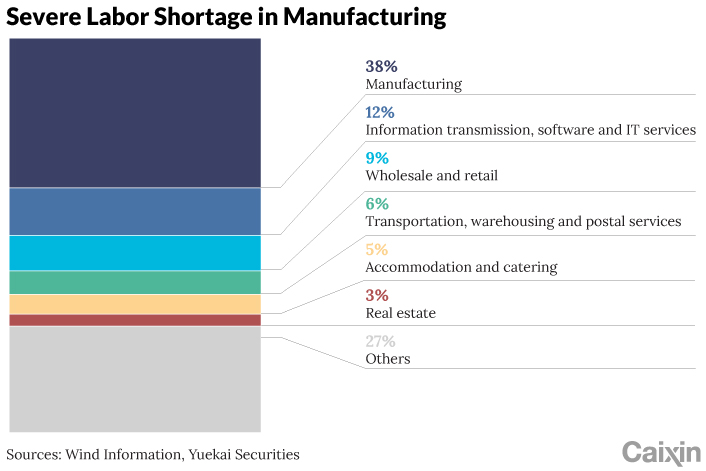

The labor shortage of the manufacturing industry accounted for 38%, while the gap for general workers with low technical requirements accounted for 55.3% in the manufacturing industry. Meanwhile, the highly skilled talent gap is widening.

The post-pandemic distribution of employment in the shared service industry has also aggravated the labor shortage in the manufacturing industry. In China, about 830 million actors participated in the sharing economy in 2020, including around 84 million individuals engaged in providing service and 6.31 million employees of digital online platforms, a year-on-year rise of 7.7% and 1.3% respectively, as estimated by the Sharing Economy Research Center under the State Information Center.

The new employment pattern in the platform-based sharing economy entails inclusivity and flexibility for workers, which not only solves the post-pandemic employment pressure but also helps to reduce the uncertainty of the employment market. Meituan, a Chinese delivery service platform, has absorbed many secondary workers during the pandemic. According to the Report on the Employment of Meituan Riders released by the Meituan Research Institute, over 35% of delivery riders used to work in factories.

|

Outlook for China’s exports

As we look into the future, exports will gradually drop to pre-pandemic levels from the pandemic high. Given the gradual rebound in industrial production and de-China-ization in the global industrial chain, it is inevitable that China’s exports will see a marginal decline from the current high level.

This year’s unexpectedly high exports provide a window for boosting solid and sound economic growth. The resilient export is a result of China’s supply-side fiscal stimulus, which aims to ensure security in operations of both market entities and foreign trade entities, thus protecting the integrity of the supply chain amid global economic uncertainty.

There are still sources of hope.

Although the pressure of counter-globalization and de-China-ization still persists, market behaviors in some Western countries may act entirely different from what the governments and politicians wished for.

While developed countries which have gone through a period of deindustrialization find it hard to rebuild their manufacturing systems, emerging economies fail to absorb the incoming orders. Great uncertainties driven by vaccine shortages and the lack of binding force of non-drug-related COVID-19 prevention measures have prevented these emerging countries from becoming the substitutions of China.

Luo Zhiheng is deputy director of Yuekai Securities Research Institute.

Contact editor Michael Bellart (michaelbellart@caixin.com)

Download our app to receive breaking news alerts and read the news on the go.

Get our weekly free Must-Read newsletter.

- RELATED

- PODCAST

- MOST POPULAR