In Depth: Why Easing Monetary Policy Is Not Enough

“You can lead a horse to water, but you can’t make it drink” is how economist Zhong Zhengsheng describes (link in Chinese) the predicament China’s central bank has found itself in as it tries to push the country’s banks to cut interest rates and increase lending to bolster flagging economic growth.

For more than two years China’s policymakers have been urging commercial lenders to hand out more credit and reduce the cost of borrowing for millions of companies, especially small and privately owned businesses. The efforts are part of the government’s strategy to support the corporate sector amid concerns that lack of access to loans and high interest rates are holding back investment and adding to companies’ financial burden.

But much of the banking industry has been reluctant and slow to respond despite a slew of encouragement from the central bank, which has included freeing up trillions of yuan of money for lending by lowering banks’ reserve requirement ratios (RRR), changing to a new benchmark lending rate and tweaking interest rates lower.

Zhong, director of macroeconomic analysis at CEBM Group Ltd., an affiliate of Caixin Global, who used the horse analogy in a recent blog posting, said sluggish borrowing demand, banks’ declining profit growth and their unwillingness to cut loan rates are all hurdles to the effectiveness of monetary policy.

The problems facing the central bank in getting its horse to drink are myriad, according to economists and bankers interviewed by Caixin. Demand for loans is sluggish as companies face a dearth of good investment opportunities and as they hunker down amid the slowdown in economic growth. Weaker domestic demand is squeezing profits and increasing the risk that companies will default on their loans.

‘Big risks’

From the banks’ perspective, there is a lack of suitable projects that meet their criteria and can generate enough cash to meet their repayment obligations, and as the economy slows, many companies are borrowing money just to keep their businesses going rather than to expand. There is also concern that boosting lending to more risky smaller companies could lead to higher nonperforming loans (NPLs) which would hurt banks’ performance under the PBOC’s quarterly Macro-Prudential Assessment (MPA), a framework that evaluates banks across a range of criteria such as bad debts, exposure to credit risk and capital adequacy.

Lending to small companies “carries big risks, and it’s really not easy to do,” a manager in the credit department of a bank based in Shandong province said. “We want to lend, but we are in a desert. There are very few high-quality companies looking for loans that meet our lending criteria. Other companies are actively deleveraging and just don’t want to borrow.”

Banks’ own profit growth is slowing which has made them less willing to cut lending rates without lowering savings rates because it would mean sacrificing profit margins. But it’s difficult for them to reduce savings rates because competition among banks for deposits is so intense. They have also resisted cutting borrowing costs to customers because the PBOC, until recently, hadn’t cut the rate it charges lenders who borrow via instruments such as the Medium-term Lending Facility (MLF).

And at a time of slowing growth and rising default risks, banks have also been unwilling to see a reduction in what’s known as their risk premium, the higher return they demand for lending to risky customers compared with the return they know they would get from using the money to invest in risk-free assets such as government bonds.

Changes in economic policy usually take time to feed through into the economy, and some analysts say that a cut in lending rates can take months to have a real, visible impact on activity. In China, where the central bank acknowledges there are inefficiencies that prevent monetary policy decisions from influencing aggregate demand, interest rates and lending, the impact of lower borrowing costs is even harder to quantify.

Banks, which are among the first to be affected by monetary policy changes, need time to adapt, one senior banker said. “Adjusting credit is related a host of factors — the bank’s own risk management and credit control capabilities, its customer acquisition strategy, its loan pricing systems and constraints on its own capital,” the banker, who spoke on condition of anonymity, told Caixin.

The campaign to boost lending and lower interest rates began in mid-2018 after the government eased up on a two-year deleveraging campaign aimed at reining in surging debt and reducing financial risks in the economy.

Lending targets

Since April 2018, the PBOC has lowered banks’ reserve requirement ratios (RRR) seven times, the most recent being a phased reduction announced in September. These cuts released funds totalling more than 5 trillion yuan for lending, with some specifically targeted at helping smaller companies, a segment of the economy that has traditionally found it hard to get funding.

Banks were set targets for boosting lending to small and midsized enterprises (SMEs) — this year the goal was for a 30% increase for the five largest state-owned banks and a 1 percentage point decline (link in Chinese) in average borrowing costs for SMEs.

In October 2018 the central bank unveiled what Governor Yi Gang described as a “three arrows” strategy to tackle the financing difficulties of private companies, targeting bank loans, debt and equity financing. This included lowering the interest rate on loans small banks get from the central bank, known as the relending rate, and raising relending and rediscount quotas, to encourage more credit to flow to private companies.

PBOC data show that annual growth in outstanding medium- and long-term (MLT) loans to companies has slowed from 15.9% in 2017 to 11.8% in 2018. At the end of October, the growth rate slowed to 10% from the end of 2018. New MLT loans to companies in the first 10 months of 2019 actually fell from the year earlier period to 5.06 trillion yuan from 5.07 trillion.

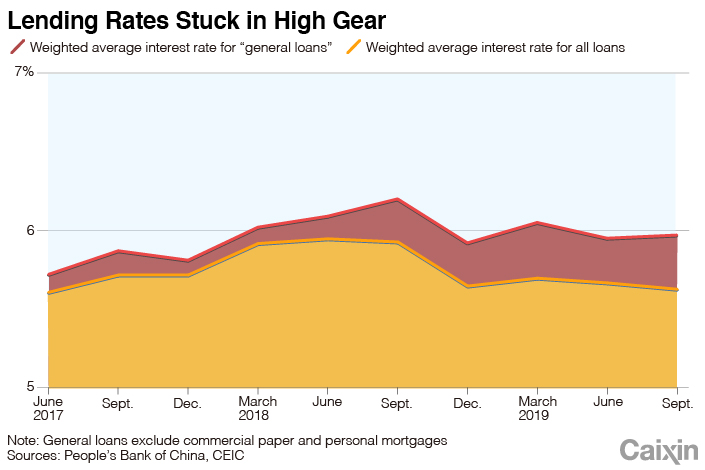

But bank lending rates remained stubbornly high, even though some economists said the surge in liquidity should have resulted in lower rates.

|

Government policies do appear to have had an impact on credit to SMEs. A PBOC report in October showed that the outstanding inclusive loans for SMEs — defined as those to businesses with less than 10 million yuan of credit — stood at 11.3 trillion yuan at the end of September, 23.3% higher than a year earlier. But the surge seems to have petered out in the third quarter, with the growth rate just 0.8 percentage points higher than at the end of June.

Li Junfeng, director of the inclusive finance department at the China Banking and Insurance Regulatory Commission, said in November that the lending rate (link in Chinese) for new inclusive finance loans fell from an average of 7.39% in 2018 to 6.75% in the third quarter of 2019.

The PBOC had refrained from following other central banks around the world in cutting borrowing costs to bolster slowing economic growth. But in August it finally bit the bullet when it completed a long-awaited overhaul of the interest-rate system to make it more market driven. The change involved banks switching to use the national Loan Prime Rate (LPR) to price their loans rather than the old benchmark interest rate system that the PBOC has been moving away from for several years.

Read more

Four Things to Know About How Loans Now Get Priced in China

Rate-cutting cycle

The shift led to an immediate reduction in rates. The first LPR announced under the new mechanism was 4.25%, down from 4.31% previously and lower than the old benchmark one-year lending rate of 4.35%. The new system raised expectations that further cuts would soon follow and they did, albeit by small steps. In November, several interest rates on different money-market instruments of various maturities were lowered by 5 basis points.

The interest rate on the one-year MLF, which banks use to determine their own internal LPR, was cut for the first time since 2016 to 3.25%; the rate on the seven-day reverse repo, an important interbank market tool used by the PBOC to control liquidity, was lowered to 2.5%, the first reduction in four years. As a result of the decline in the borrowing cost for MLF, the national LPR interest rates on one-year and five-year-plus loans fell to 4.15% and 4.8% respectively at their monthly adjustment on Nov. 20.

The PBOC made the cuts in spite of a surge in inflation caused by a nationwide outbreak of swine fever, which has sent pork prices through the roof and driven the consumer price index to its highest in eight years. But with prices other than meat still mostly below the government’s annual inflation ceiling of around 3%, supporting the economy has taken precedence.

Many analysts say the PBOC has now entered a mild rate-cutting cycle. There is still room for more interest rate cuts, but how much will depend on how the economy is performing and the external environment, said Lian Ping, chief economist at Bank of Communications, referring to factors including the trade war with the U.S.

The question now is how much scope there is to keep cutting interest rates not only from a macroeconomic perspective, where the narrowing of the spread between Chinese and U.S. interest rates could lead to capital outflows and pressure on the yuan to depreciate, but also from the perspective of banks. Lenders are suffering from declining growth in profits, higher nonperforming loans, and the need to strengthen their balance sheets as required by the central bank’s MPA.

Even if borrowing costs do fall, how much additional room is there to increase lending given constraints on both the demand and supply sides, and especially in view of already high local government debt levels and controls on lending to the real estate industry — traditionally two major drivers of credit.

The PBOC and Governor Yi have hinted that further interest-rate cuts may be in the cards as policymakers step up their response to the economic slowdown through the use of counter-cyclical policies, which work to support or stimulate the economy in a downturn. A meeting of the Politburo, the Communist Party’s top decision-making body, on Friday reiterated that the government should adopt “counter-cyclical adjustment tools” as part of its policy framework.

Monetary-policy limitations

Economists from Macquarie Securities Ltd. say that cutting rates will not be enough to stabilize the economy.

“For growth to bottom, credit growth has to pick up first, but it’s constrained by a lack of credit demand at this stage,” Macquarie economists led by Larry Hu wrote in a Nov. 18 research note. “Like the case in 2012 and 2015, cutting rates could only do so much to boost credit demand. The ultimate solution is to create demand artificially from infra(structure) and/or property.”

Hu from UBS also doubts that the PBOC’s measures will spur lending. “It’s just a fact that companies are unwilling to borrow when the economic cycle turns down, and it’s something that happens not just in China but in other countries too,” Hu said.

Wang Yifeng, chief banking analyst at Everbright Securities, suggests one way to strengthen the impact of counter-cyclical adjustments would be for the PBOC to adjust some of the parameters in the MPA to encourage lending for investment.

China’s policymakers and economists realize that monetary policy has limitations in terms of its effectiveness in boosting lending and stimulating the economy. Governor Yi wrote in an article published on Dec. 1 that China will continue to refrain from large-scale easing, citing “worse-than-expected” results from the unprecedented monetary stimulus by some developed countries after the financial crisis in 2008.

Economic growth is ultimately determined by fundamental structural factors, such as an aging population, improvements in technology, and economic globalization, none of which can be changed by monetary policy, Yi said. He also underscored the need for a proactive fiscal policy to promote structural reform and cut taxes and fees.

Economists are calling for more structural reforms (link in Chinese) to boost the economy, including allowing more rural residents to move to urban areas and enjoy the same welfare benefits as city residents, protecting intellectual property, and breaking up monopolies to allow more competition in industries including energy, transport and telecommunications, which are dominated by large state-owned enterprises.

A previous version of this story gave the incorrect time period over which MLT loans grew 10%. It was at the end of October.

Contact reporter Guo Yingzhe (yingzheguo@caixin.com)

Caixin Global has officially launched Caixin CEIC Mobile, a mobile-only version of a world-class platform for macroeconomic and microeconomic data.

From now on, all users can enjoy a one-month free trial on the Caixin App through December 2019. If you’re using our App, click here. If you haven’t downloaded the App, click here.

- RELATED

- PODCAST

- MOST POPULAR